If you are a homeowner in Houston, TX, you have likely watched the real estate headlines with a mix of curiosity and caution. With the shifting economic landscape, fluctuating interest rates, and rising property values across Texas, one question we hear constantly at Peyton Mortgage is: “Is refinancing my mortgage worth it right now?”

If you are a homeowner in Houston, TX, you have likely watched the real estate headlines with a mix of curiosity and caution. With the shifting economic landscape, fluctuating interest rates, and rising property values across Texas, one question we hear constantly at Peyton Mortgage is: “Is refinancing my mortgage worth it right now?”

The answer isn’t a simple “yes” or “no.” It depends entirely on your specific financial goals, your current equity position, and how long you plan to stay in your home. While the days of rock-bottom pandemic interest rates are behind us, refinancing remains a powerful financial tool for many homeowners. Whether you are looking to lower your monthly payment, tap into your home’s equity for renovations, or consolidate high-interest debt, understanding the mechanics of a refinance is crucial.

In this guide, we will break down the math, the market conditions, and the local factors affecting mortgage refinancing in Houston to help you decide if it is the right move for your financial future.

Understanding the “Why”: Common Reasons to Refinance

Before diving into the “right now,” it is essential to understand the strategic reasons homeowners choose to refinance. Refinancing involves replacing your existing mortgage with a new one, usually with different terms. Here are the primary drivers:

1. Lowering Your Interest Rate

This is the most traditional reason to refinance. If current market rates are lower than the rate on your existing note, refinancing can reduce your monthly interest costs. Even a reduction of 0.50% to 0.75% can result in significant savings over the life of the loan.

2. Cash-Out Refinancing (Debt Consolidation)

For many Houston homeowners, this is currently the most compelling reason to refinance. A cash-out refinance allows you to borrow more than you owe on your home and pocket the difference in cash.

With credit card interest rates and personal loan rates climbing, using your home equity to pay off high-interest debt can be a game-changer. Even if your new mortgage rate is slightly higher than your old one, the blended rate of your total debt load often drops significantly, improving your monthly cash flow.

3. Shortening the Loan Term

If you are in a strong financial position, you might refinance from a 30-year fixed mortgage to a 15-year fixed mortgage. While your monthly payment might increase, you will pay off the home faster and save a substantial amount in total interest.

4. Eliminating Private Mortgage Insurance (PMI)

If you purchased your home with less than a 20% down payment, you are likely paying PMI. However, property values in Houston have risen over the last few years. If your home’s value has increased enough to give you 20% equity, refinancing can remove that PMI requirement, instantly lowering your monthly bill.

The Math: Calculating Your Break-Even Point

Determining if a refinance is “worth it” requires a calculation known as the break-even point. This is the point in time when the savings from your new mortgage outweigh the costs of obtaining it.

Refinancing comes with closing costs, which typically range from 2% to 5% of the loan amount. These costs include appraisal fees, title insurance, and lender fees.

How to Calculate It:

Total Closing Costs ÷ Monthly Savings = Months to Break Even

For example, let’s assume the following scenario:

- Refinance Closing Costs: $4,000

- Monthly Savings: $200

- Calculation: $4,000 ÷ $200 = 20 months

In this scenario, it takes 20 months to recoup the cost of the refinance. If you plan to stay in your home for five years (60 months), refinancing is a smart financial move. If you plan to sell next year, it would not be worth it.

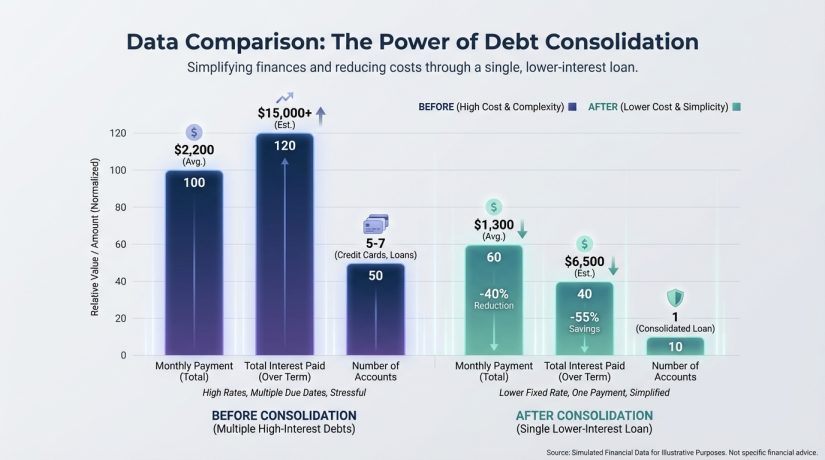

Data Comparison: The Power of Debt Consolidation

| Scenario | Mortgage Debt | Credit Card Debt | Total Monthly Payment | Net Monthly Savings |

|---|---|---|---|---|

| Current Situation | $2,000/mo (4% rate) | $800/mo (22% rate) | $2,800 | — |

| After Cash-Out Refi | $2,300/mo (6.5% rate) | $0 (Paid off) | $2,300 | $500/mo Saved |

*Note: This is a hypothetical example for illustrative purposes. Actual rates and payments vary based on credit score and loan-to-value ratio. Contact Peyton Mortgage for a custom rate quote.

Local Insight: Refinancing in Houston, TX

Real estate is local, and refinancing rules can vary by state. Working with a local expert like Roger Young at Peyton Mortgage ensures you navigate Texas-specific regulations correctly.

Texas Cash-Out Refinance Rules (Section 50(a)(6))

In Texas, the total amount of all loans secured by the home cannot exceed 80% of the home’s fair market value. This means you must retain at least 20% equity in your property after the cash-out transaction. While this limits how much cash you can pull out compared to other states, it also ensures homeowners do not become over-leveraged.

Houston Property Values

The Houston housing market has seen robust appreciation. Many homeowners who bought in neighborhoods like The Heights, Katy, Cypress, or Sugar Land just a few years ago may be sitting on significantly more equity than they realize. This “hidden” wealth is what makes refinancing viable, even in a higher-rate environment.

Is “Right Now” the Right Time?

We often hear the phrase, “Marry the house, date the rate.” While rates fluctuate, your home is a long-term asset. Waiting for the “perfect” bottom-of-the-market rate can sometimes result in missed opportunities, especially if you are currently carrying high-interest consumer debt.

Refinancing might be worth it RIGHT NOW if:

- Your credit score has improved significantly since you bought your home.

- You have variable-rate debt (HELOCs or credit cards) that is becoming unmanageable.

- You want to switch from an Adjustable-Rate Mortgage (ARM) to a Fixed-Rate Mortgage for stability.

- You need to fund a major home renovation to increase your property value further.

However, it might be better to wait if you plan to move within the next 12-24 months or if the closing costs exceed your potential savings over your residency period.

The Peyton Mortgage Advantage

At Peyton Mortgage, we don’t just sell loans; we build financial strategies. We understand the Houston market because we live and work here. When you call us, you aren’t getting a call center; you are getting personalized advice.

We will help you run the numbers on our mortgage calculator and provide a transparent breakdown of costs versus savings so you can make an educated decision.

Frequently Asked Questions (FAQs)

1. How much does it cost to refinance a mortgage in Texas?

Closing costs for a refinance typically range between 2% and 5% of the loan amount. In Texas, these costs cover the appraisal, title search, title insurance, and lender fees. However, some lenders offer “no-closing-cost” refinances where the costs are rolled into the loan rate.

2. Does refinancing hurt my credit score?

Initially, yes, but only slightly. When you apply, the lender performs a hard inquiry, which may drop your score by a few points. However, if you use the refinance to pay off high-balance credit cards, your credit utilization ratio will drop, which often boosts your credit score significantly in the long run.

3. How long does the refinancing process take?

On average, a refinance takes 30 to 45 days from application to closing. The timeline depends on how quickly the appraisal can be completed and how fast you provide the necessary documentation. At Peyton Mortgage, we strive to make the loan process as efficient as possible.

4. Can I refinance if I have bad credit?

While a higher credit score generally secures a lower interest rate, options exist for borrowers with less-than-perfect credit. FHA refinances and VA Interest Rate Reduction Refinance Loans (IRRRL) have more lenient credit requirements. Contact us to discuss your specific situation.

5. How often can I refinance my home?

There is no legal limit to how often you can refinance, but many lenders have a “seasoning” requirement, typically asking that you hold the original loan for at least six months before refinancing again. In Texas, once you complete a cash-out refinance (Section 50(a)(6)), you must wait 12 months before you can execute another cash-out refinance on the same property.

Ready to Explore Your Refinancing Options?

Don’t leave your financial future to guesswork. Whether you want to lower your monthly payments or access your home’s equity, Roger Young and the team at Peyton Mortgage are here to guide you through every step of the process.

We serve homeowners across Houston, TX, providing competitive rates and honest advice.