Welcome to Peyton Mortgage, your premier destination for innovative real estate financing in Houston, Texas. If you are a real estate investor looking to expand your portfolio without the strict personal income requirements of traditional mortgages, a Debt Service Coverage Ratio (DSCR) loan might be the perfect solution for you. Led by mortgage expert Roger Young, Peyton Mortgage specializes in helping investors leverage the cash flow of their rental properties to secure fast, reliable, and scalable funding.

Traditional mortgage lending often focuses heavily on personal income stability, W-2s, and debt-to-income (DTI) ratios. As we often remind our clients, while conventional loans dictate that personal income stability matters more than rate shopping, DSCR loans flip the script. With a DSCR loan, the property’s income stability is what truly matters. We look at the cash flow generated by your investment property to qualify you for the loan, allowing you to bypass personal income verification entirely.

What is a Debt Service Coverage Ratio (DSCR) Loan?

A Debt Service Coverage Ratio (DSCR) loan is a specialized type of non-QM (Non-Qualified Mortgage) investment property loan designed specifically for real estate investors. Instead of using your personal tax returns, pay stubs, or employment history to qualify for the mortgage, lenders use the DSCR formula to determine if the property generates enough rental income to cover the mortgage payments and associated expenses.

In simple terms, if the property pays for itself, it qualifies for the loan. This makes DSCR loans incredibly powerful for self-employed investors, freelancers, retirees, or any investor who has reached the limit of conventional loans they can hold in their personal name.

The Power of Cash Flow Over Personal Income

Real estate investors frequently face roadblocks with traditional lenders because traditional underwriting is designed for primary homebuyers. If you write off expenses on your taxes to minimize your tax burden (as most savvy business owners do), your “on-paper” personal income may appear too low to qualify for conventional financing. DSCR loans eliminate this hurdle. By focusing exclusively on the gross rental income of the property compared to its debt obligations, Peyton Mortgage empowers Houston investors to keep acquiring properties.

How to Calculate DSCR for Houston Investment Properties

Understanding how the Debt Service Coverage Ratio is calculated is crucial for any real estate investor. The formula is straightforward:

DSCR = Gross Operating Income / Total Debt Service (PITI)

- Gross Operating Income: The total gross rental income generated by the property. This is usually determined by a lease agreement currently in place, or by an appraiser’s estimate of market rent (Form 1007) if the property is vacant.

- Total Debt Service (PITI or PITIA): The total monthly cost of the loan, which includes Principal, Interest, Taxes, Insurance, and sometimes Homeowners Association (HOA) fees.

Understanding the DSCR Ratio Numbers

When you divide the rental income by the mortgage expenses, you get a ratio. Here is what those numbers mean to lenders:

- DSCR > 1.0 (Positive Cash Flow): A ratio greater than 1.0 means the property generates more income than it costs to maintain the debt. For example, a DSCR of 1.25 means the property generates 25% more income than the monthly mortgage payment. Most lenders prefer a minimum DSCR of 1.15 to 1.25.

- DSCR = 1.0 (Break-Even): A ratio of exactly 1.0 means the rental income perfectly covers the debt service. The property is breaking even. Some aggressive DSCR programs will lend on a 1.0 ratio.

- DSCR < 1.0 (Negative Cash Flow): A ratio below 1.0 means the property does not generate enough rent to cover the mortgage. For instance, a 0.80 DSCR means the rent only covers 80% of the mortgage. While harder to finance, Peyton Mortgage does have access to select “No Ratio” or sub-1.0 DSCR programs for investors with excellent credit and large down payments who are banking on property appreciation or future rent increases.

A Real-World Houston DSCR Example

Let’s say you are looking to purchase a single-family rental property in Katy, TX, or Sugar Land, TX.

The estimated monthly rental income (Gross Income) is $2,500.

Your proposed monthly mortgage payment, including taxes and insurance (PITI), is $2,000.

$2,500 / $2,000 = 1.25 DSCR

A ratio of 1.25 is considered strong and will easily meet the underwriting guidelines for most DSCR loan programs offered by Peyton Mortgage.

Why Real Estate Investors in Houston Choose DSCR Loans

The Houston real estate market is dynamic, fast-paced, and filled with opportunity. To compete, investors need agile financing. Here are the primary benefits of choosing a DSCR loan through Peyton Mortgage:

1. No Personal Income Verification or DTI Limits

Leave your W-2s, 1040s, and pay stubs in the filing cabinet. Because qualification is based on property cash flow, your personal Debt-to-Income (DTI) ratio is entirely irrelevant. This is the ultimate solution for self-employed borrowers.

2. Unlimited Portfolio Scaling

Fannie Mae and Freddie Mac place strict limits on the number of financed investment properties you can hold (typically capped at 10). DSCR loans have no such limits. Whether you are buying your first rental or your fiftieth, DSCR loans allow you to scale your portfolio infinitely.

3. Close in the Name of an LLC or Corporation

Asset protection is vital for real estate investors. Conventional loans usually require you to close in your personal name. DSCR loans, however, are commercial-purpose loans, meaning you can easily close in the name of a Limited Liability Company (LLC), S-Corp, or C-Corp, shielding your personal assets from potential liabilities.

4. Faster Closing Times

Because the underwriter does not have to sift through hundreds of pages of personal tax returns and bank statements to verify income, the underwriting process is significantly streamlined. This allows Peyton Mortgage to close your DSCR loans faster, helping you win competitive bids in the Houston market.

5. Perfect for Short-Term Rentals (Airbnb / VRBO)

Houston is a massive hub for medical professionals, corporate travelers, and tourists, making it a lucrative market for short-term rentals. Many DSCR lenders allow you to use projected short-term rental income (often via AirDNA data) rather than standard long-term lease estimates, allowing you to qualify for higher loan amounts based on the higher yield of an Airbnb property.

Houston, TX: A Prime Market for DSCR Real Estate Investing

Location is everything in real estate, and Houston, Texas, represents one of the strongest investment markets in the United States. At Peyton Mortgage, we understand the local nuances of Harris County and the surrounding metropolitan areas.

Houston boasts a massive, growing population, a diverse economy rooted in energy, healthcare (the Texas Medical Center), aerospace, and technology. This economic stability drives constant demand for rental housing. Furthermore, Texas is a landlord-friendly state with no state income tax, making your cash-flowing properties even more profitable.

Whether you are investing in multi-family units in Montrose, single-family homes in Cypress, or short-term rentals near the Galleria or NRG Stadium, utilizing a DSCR loan allows you to capture the high rental yields the Houston market has to offer.

DSCR Loan Requirements and Qualifications

While DSCR loans are easier to qualify for than conventional loans in terms of income documentation, they still have specific requirements to mitigate the lender’s risk. When you work with Roger Young at Peyton Mortgage, we will guide you through these requirements:

- Credit Score: A minimum FICO score of 620 is typically required, though scores of 680 or higher will unlock the best interest rates and highest Loan-to-Value (LTV) ratios.

- Down Payment / Equity: Expect to put down a minimum of 15% to 20% for a purchase. If you are refinancing, lenders generally allow up to 75% to 80% LTV.

- DSCR Ratio: Most programs require a minimum DSCR of 1.15 to 1.25. However, we have specialized programs for ratios down to 1.0, and even negative cash-flow properties for highly qualified borrowers.

- Property Types: DSCR loans can be used for single-family residences (SFR), 2-4 unit multi-family properties, townhomes, and warrantable/non-warrantable condos. Some programs also allow for 5-8 unit commercial residential properties.

- Reserves: Lenders typically require you to show 3 to 6 months of PITI in liquid reserves to ensure you can cover the mortgage in the event of a vacancy.

Comparing Financing Options: DSCR vs. Conventional Investment Loans

To help you understand why a DSCR loan might be the superior choice for your investment strategy, we have created a comparison table highlighting the key differences between DSCR loans and conventional investment property loans.

| Feature | DSCR Loan | Conventional Investment Loan |

|---|---|---|

| Income Verification | None (Based on property cash flow) | Extensive (W-2s, Tax Returns, Pay stubs) |

| DTI Limit | No DTI calculated | Strictly capped (usually around 45-50%) |

| Entity Borrowing | Allowed (LLCs, Corps, Trusts) | Not allowed (Must close in personal name) |

| Property Limit | Unlimited | Capped (Maximum of 10 financed properties) |

| Underwriting Speed | Fast and streamlined | Slow and document-heavy |

| Interest Rates | Slightly higher than conventional | Lower, standard market rates |

| Short-Term Rentals | Highly flexible (AirDNA data often accepted) | Difficult (Usually requires 2 years of tax returns showing STR income) |

Cash-Out Refinancing with a DSCR Loan

DSCR loans are not just for purchasing new properties; they are an incredible tool for unlocking trapped equity in your existing portfolio. If you own rental properties in Houston that have appreciated in value, or if you have completed the “BRRRR” method (Buy, Rehab, Rent, Refinance, Repeat), a DSCR cash-out refinance is your next step.

With a DSCR cash-out refinance from Peyton Mortgage, you can pull cash out of your property up to 75% or 80% of its newly appraised value. Because the new loan is still based on the property’s rental income, you do not have to worry about your personal income qualifying for the higher loan amount. You can use the tax-free cash out to fund renovations, purchase additional investment properties, or increase your liquid cash reserves.

The Peyton Mortgage Streamlined Process

Securing a DSCR loan in Houston should not be a headache. Roger Young and the team at Peyton Mortgage have refined the lending process to be as efficient and transparent as possible. Here is what you can expect when you partner with us:

Step 1: Discovery and Strategy Session

Step 2: Property Cash Flow Analysis

We will review the property’s current or projected rental income and calculate the estimated PITI to determine the DSCR ratio. We will provide you with a clear breakdown of your expected interest rate, down payment requirements, and closing costs.

Step 3: Application and Documentation

Step 4: Appraisal and Rent Schedule

We will order a specialized appraisal that includes a Form 1007 (Single-Family Comparable Rent Schedule) or Form 1025 (Small Residential Income Property Appraisal Report). This verifies the market value of the home and the fair market rent, which is the cornerstone of DSCR underwriting.

Step 5: Clear to Close

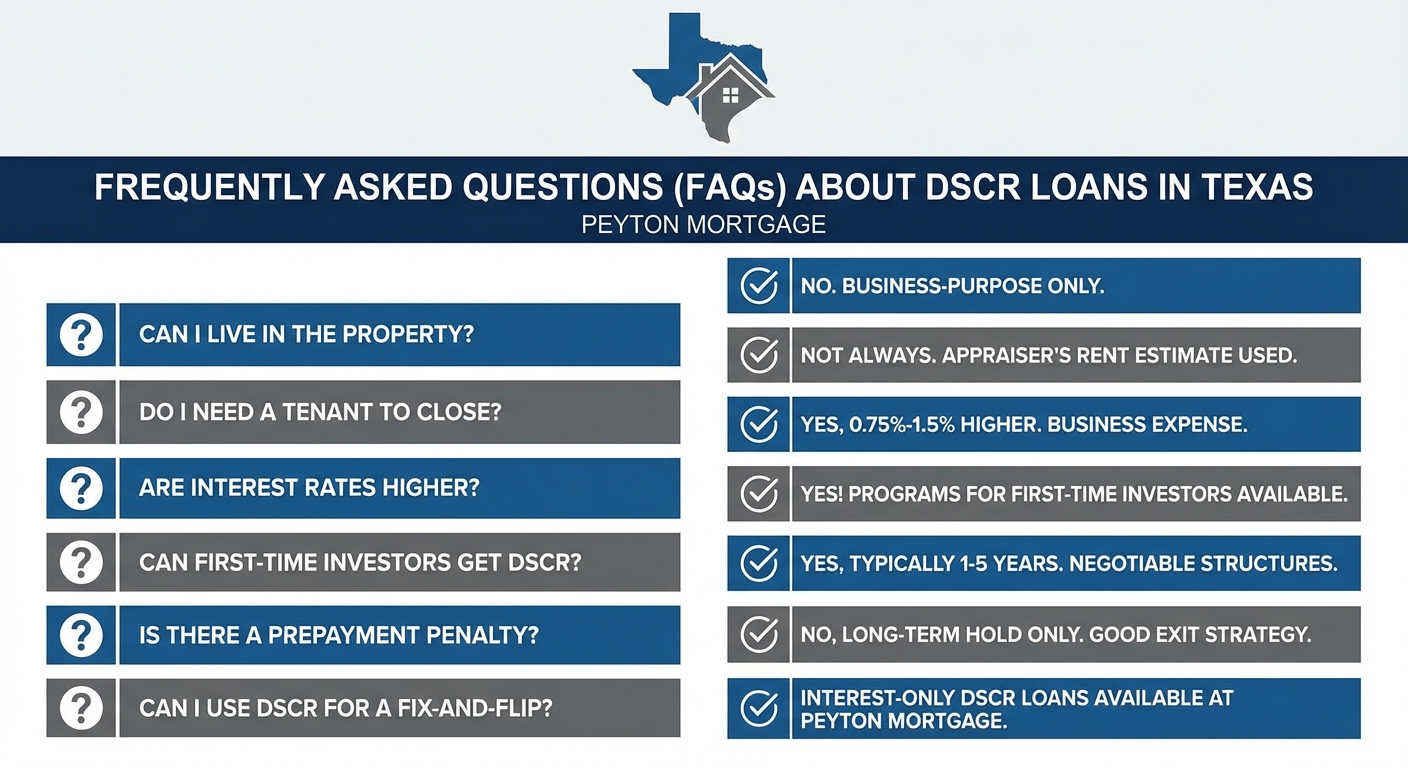

Frequently Asked Questions (FAQs) About DSCR Loans in Texas

Can I live in the property financed by a DSCR loan?

No. DSCR loans are strictly for business-purpose, non-owner-occupied investment properties. You cannot live in the property for any portion of the year. If you are looking for a primary residence loan, Peyton Mortgage offers a wide variety of conventional, FHA, and VA loans.

Do I need to have a tenant in place to close a DSCR loan?

Not necessarily. While having a signed lease is helpful, it is not always required. If the property is vacant, the lender will use the appraiser’s estimate of market rent (the 1007 Rent Schedule) to calculate the DSCR ratio.

Are interest rates higher on DSCR loans?

Yes, DSCR loan interest rates are typically 0.75% to 1.5% higher than conventional primary residence rates. This is because they carry slightly more risk for the lender due to the lack of personal income verification. However, for investors, the ability to scale and protect assets via an LLC far outweighs the slightly higher rate, which is a tax-deductible business expense.

Can a first-time real estate investor get a DSCR loan?

Yes! While some lenders require a history of owning investment properties, Peyton Mortgage has access to DSCR programs specifically designed for first-time investors. You may face a slightly lower maximum LTV (e.g., 75% instead of 80%), but it is entirely possible to start your investing journey with a DSCR loan.

Is there a prepayment penalty on DSCR loans?

Most DSCR loans do come with a prepayment penalty (PPP), typically lasting for the first 1 to 5 years of the loan. This is standard for commercial-style lending. However, the structure of the PPP is often negotiable. We can help you weigh the pros and cons of different PPP structures to find the best fit for your exit strategy.

Can I use a DSCR loan for a fix-and-flip?

DSCR loans are designed for long-term hold strategies (30-year fixed, ARMs, or Interest-Only loans) where the property is generating rental income. They are not suitable for fix-and-flips, as flipping requires short-term bridge or hard money financing. However, DSCR is the perfect exit strategy to refinance out of a hard money loan once the rehab is complete and the property is rented.

Does Peyton Mortgage offer Interest-Only DSCR loans?

Yes. Interest-only (IO) DSCR loans are incredibly popular among Houston investors. By paying only the interest for the first 10 years of a 30-year or 40-year term, your monthly payment is significantly lower, which maximizes your monthly cash flow and increases your DSCR ratio, making it easier to qualify.

Trust Peyton Mortgage for Your Houston Investment Financing

At Peyton Mortgage, we pride ourselves on being more than just a mortgage broker; we are your strategic lending partner. We understand that real estate investing is a business, and your financing should operate with the same level of professionalism, speed, and strategic foresight that you bring to your property acquisitions.

With deep roots in Houston, TX, Roger Young and the team possess the local market knowledge and the extensive network of wholesale lending partners required to secure the most competitive DSCR terms available. We navigate the complexities of non-QM lending so you can focus on what you do best: finding great properties and managing your portfolio.

Take the Next Step: Contact Peyton Mortgage Today

Are you ready to break free from the limitations of traditional mortgage lending? Stop letting personal income requirements dictate the size of your real estate portfolio. Leverage the cash flow of your properties with a Debt Service Coverage Ratio loan.

Reach out to Roger Young at Peyton Mortgage today for a free, no-obligation DSCR scenario review and rate quote.

- Contact Name: Roger Young

- Phone: 1-346-570-0846

- Email: roger@peytonmortgage.com

- Website: peytonmortgage.com

- Location: Houston, TX

Peyton Mortgage is an Equal Housing Opportunity broker. All loan programs, terms, and interest rates are subject to change without notice and subject to borrower and property qualifications. DSCR loans are for business purposes only and are not intended for consumer or owner-occupied residential use.