While fireworks, barbecues, and parades are fundamental to our 4th of July celebrations, the spirit of Independence Day runs much deeper. It’s a time to honor our history, recognize our freedoms, and celebrate the unity that defines us as a nation.

A History Worth Remembering

On July 4, 1776, the Continental Congress adopted the Declaration of Independence, marking the birth of the United States of America. This historic document, crafted by Thomas Jefferson and signed by representatives of the thirteen colonies, asserted our nation’s right to self-governance and freedom from British rule. It was a bold declaration of the values we hold dear—liberty, equality, and the pursuit of happiness.

Honoring Our Freedoms

Independence Day is a celebration of the freedoms that are foundational to our nation. The freedoms of speech, religion, and assembly, among others, are enshrined in our Constitution and Bill of Rights. These freedoms have shaped our society and continue to be the cornerstone of American democracy. By celebrating the 4th of July, we pay tribute to the vision of our Founding Fathers and the sacrifices of countless individuals who have fought to preserve these rights.

A Time for Gratitude

It is important to express gratitude for the privileges we enjoy as Americans. The freedoms and opportunities we often take for granted are the result of the hard-fought battles and unwavering determination of those who came before us. Taking a moment to appreciate this legacy fosters a sense of responsibility to protect and nurture these values for future generations.

As we light up the sky with fireworks and gather with loved ones this 4th of July, let’s remember that Independence Day is more than just a summer holiday. It’s a celebration of our history, our freedoms, and our unity. By reflecting on the significance of this day, we can truly appreciate the privileges we enjoy and commit ourselves to upholding the values that define our great nation.

Happy Independence Day! Let’s celebrate with pride and purpose. What are your favorite 4th of July traditions? Share them with us in the comments below!

Stay safe and enjoy your 4th of July!

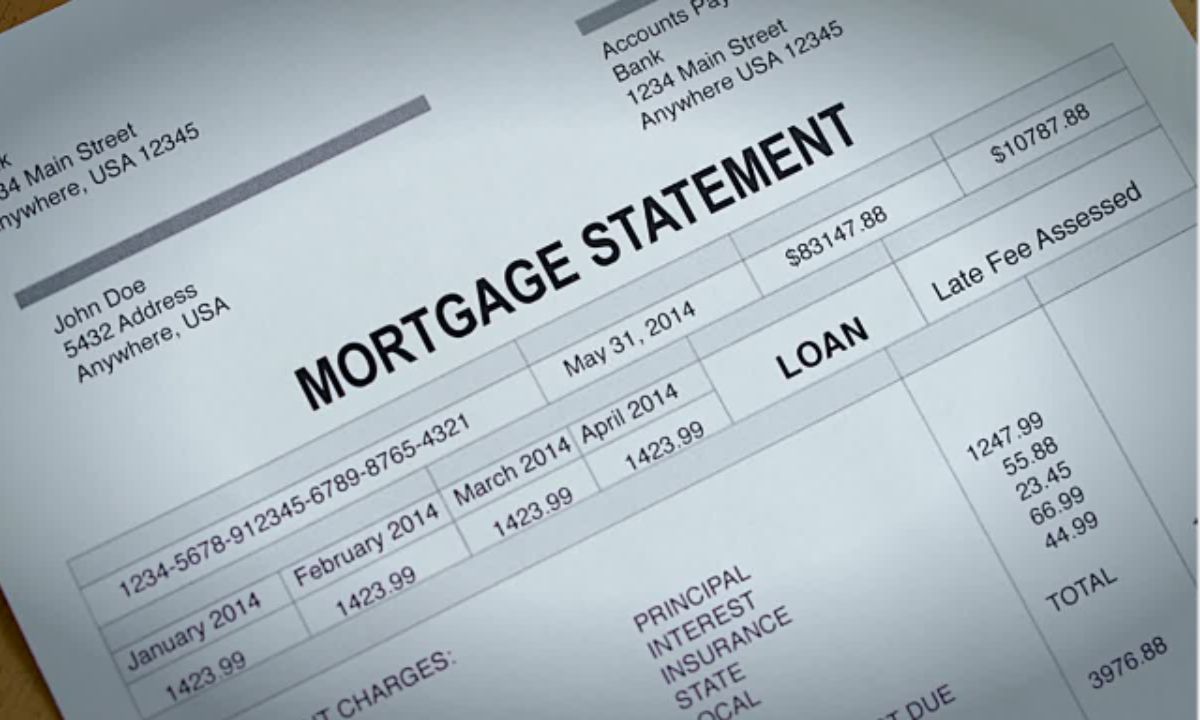

Your mortgage statement is an important document that provides detailed information about your home loan. Understanding it can help you manage your mortgage more effectively, identify potential issues early, and ensure you’re on track with your payments. Here is a list to help guide you when reading your mortgage statement, what to look for, and how to verify its accuracy.

Your mortgage statement is an important document that provides detailed information about your home loan. Understanding it can help you manage your mortgage more effectively, identify potential issues early, and ensure you’re on track with your payments. Here is a list to help guide you when reading your mortgage statement, what to look for, and how to verify its accuracy. When it comes to buying a home, you will find many mortgage options available. One of the lesser-known but potentially advantageous choices is the Graduated Payment Mortgage (GPM). Let’s discuss what GPMs are, how they work, and how they differ from other mortgage options.

When it comes to buying a home, you will find many mortgage options available. One of the lesser-known but potentially advantageous choices is the Graduated Payment Mortgage (GPM). Let’s discuss what GPMs are, how they work, and how they differ from other mortgage options.